Dog Food Market Forecast 2026-2036: Global Market to Reach USD 97.4 Billion by 2036 at 6.0% CAGR

Global dog food market growth is driven by premium nutrition, regulatory compliance, functional formulations, and rising demand for science-backed canine diets.

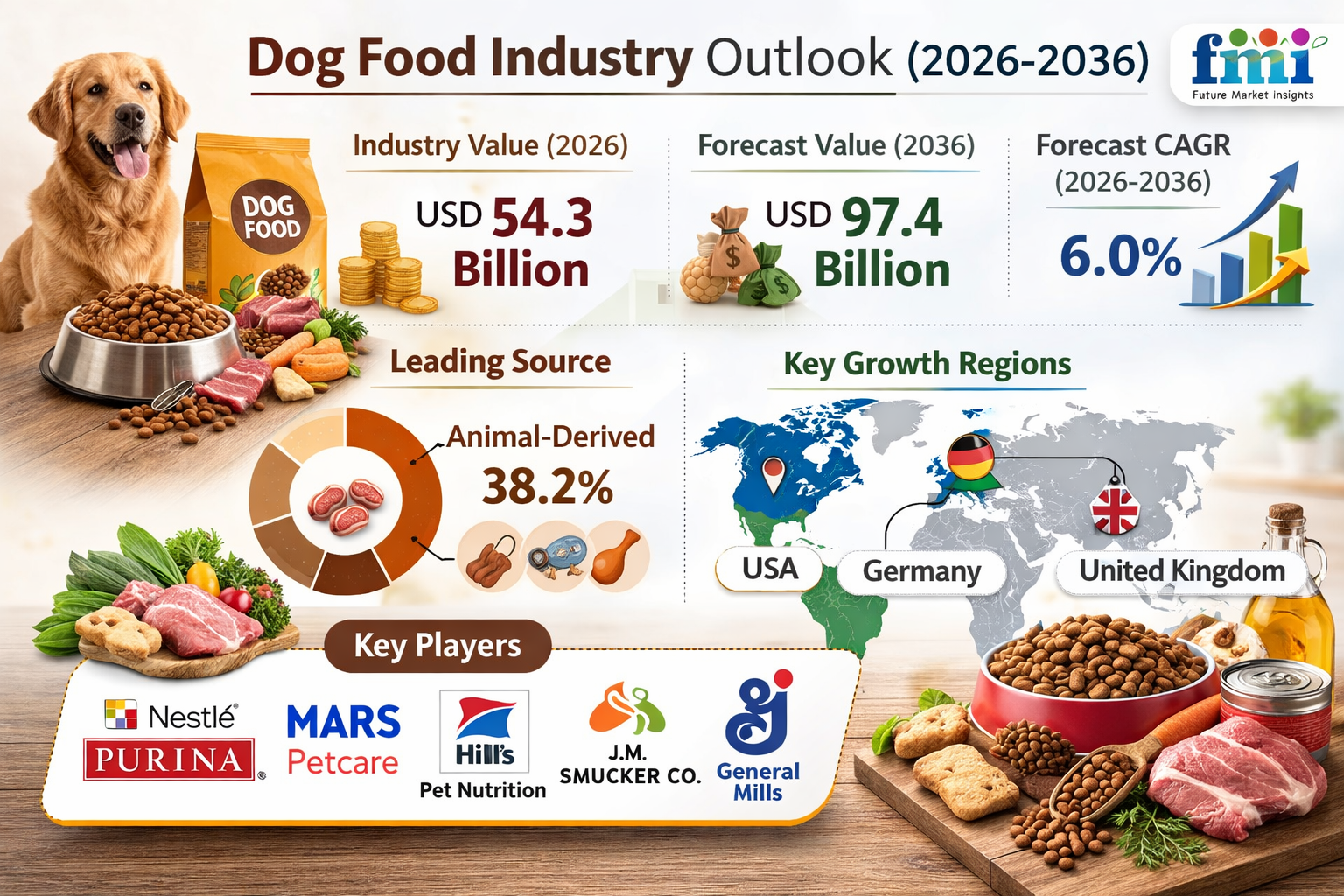

NEWARK, DELAWARE / ACCESS Newswire / February 23, 2026 / The global dog food industry is entering a decisive expansion phase, shaped by premiumization, regulatory rigor, and science-backed formulation strategies. Valued at USD 54.3 billion in 2026, the sector is projected to reach USD 97.4 billion by 2036, advancing at a CAGR of 6.0%. According to the latest assessment by Future Market Insights (FMI), sustained growth is being powered by higher per-pet spending, rapid adoption of life-stage and condition-specific formulas, and increasing consumer willingness to trade up to digestibility-focused and functionally enhanced diets.

Unlike previous growth cycles driven by flavor proliferation and marketing claims, the next decade will be defined by feed safety compliance, measurable nutritional performance, and substantiated functional positioning.

Science-Led Nutrition: From Protein Claims to Proof

Manufacturers are scaling R&D investments to validate protein quality, amino acid balance, and digestibility using structured feeding trials and controlled palatability testing. Animal-derived ingredients currently command 38.2% of total source share, reflecting continued reliance on complete-protein nutrition supported by veterinary guidance.

Production strategy is increasingly influenced by regulatory frameworks that govern ingredient selection, safety systems, and labeling clarity:

In the United States, the Food Safety Modernization Act (FSMA) preventive controls for animal food require covered facilities to maintain written food safety plans, hazard analyses, and risk-based preventive controls.

In the European Union, Regulation (EC) No 767/2009 governs feed labeling and claim presentation, while Regulation (EC) No 183/2005 enforces hygiene standards across the feed chain.

These frameworks are raising standards for traceability, contamination controls, supplier approval systems, and claim substantiation-creating competitive advantages for companies that integrate compliance into product design rather than treating it as an afterthought.

Get Access of Report Sample: https://www.futuremarketinsights.com/reports/sample/rep-gb-13961

Operational KPIs Validate Animal-Protein Adoption

Growth in animal-derived proteins is being evaluated through measurable production and quality benchmarks across the value chain. Key performance indicators include:

COGS, yield percentage, and OEE to measure production efficiency, especially for freeze-dried and fresh-meat lines

CSAT and NPS to capture palatability-driven repeat purchases

Safety incident rate and compliance rate to monitor audit readiness and hygiene controls

Inventory turnover and waste percentage to manage cold-chain exposure and shelf-life risks

Energy consumption per unit to assess sustainability impact of cooking, drying, and refrigeration

Manufacturers that balance nutritional performance with operational discipline are expected to capture disproportionate value over the next decade.

Segmentation Drives Targeted Growth

The dog food market is structurally segmented by source, product type, pet age, packaging format, and distribution channel-reflecting a shift from generic feeding to targeted life-stage nutrition.

Kibble leads product applications with a 42.6% share, favored for shelf stability, dental health benefits, and convenience.

Pet stores dominate distribution with a 35.4% share, supported by specialized retail guidance and premium positioning.

Animal-derived sources retain leadership at 38.2%, anchored in essential amino acid completeness and digestibility performance.

Granular segmentation allows manufacturers to tailor offerings for veterinary clinics, specialty retailers, and mainstream outlets while aligning formulations with evolving veterinary benchmarks.

Regional Outlook: Premiumization Shapes Mature Markets

Adoption trends vary by geography, with established markets prioritizing validated nutrition and sustainability credentials.

United States (4.3% CAGR): Growth is underpinned by strong pet spending capacity and expanding insurance coverage. With dogs representing over three-quarters of insured pets, veterinarian-guided nutrition adoption is accelerating. Preventive controls under federal regulations further reinforce investments in quality systems that justify premium pricing.

Germany (3.9% CAGR): A large pet base and structured prepared-food ecosystem support steady expansion. Sustainability preferences and rising organic farming participation influence ingredient sourcing and labeling claims.

United Kingdom (2.8% CAGR): Strong household penetration and stringent feed safety oversight reinforce demand for compliant, well-documented nutrition lines.

Canada (3.2% CAGR): Growth is supported by rising dog ownership and channel expansion, with value gains reflecting both pricing and trading up into higher-quality formulations.

France (2.6% CAGR): High reliance on prepared industrial pet food sustains structural demand, while retail-driven premium shelf expansion shapes competition.

Functional Nutrition and Humanization Accelerate Premium Sales

Pet humanization continues to elevate expectations around ingredient transparency, freshness cues, and "human-grade" positioning. Functional nutrition-targeting digestion, daily vitality, and condition-specific outcomes-has emerged as a measurable growth engine.

However, commercialization is shaped by evolving regulatory oversight, particularly around probiotic and functional claims. Companies must substantiate digestive and microbiome benefits with robust data to mitigate compliance risks and maintain label credibility.

Sustainability Innovation Gains Strategic Importance

Environmental reporting frameworks are influencing manufacturing development decisions. Standardized footprint measurement approaches in Europe, including Product Environmental Footprint (PEF) methodology, are pushing manufacturers toward improved supplier transparency, primary data collection, and auditable documentation.

Process optimization-especially in extrusion, freeze-drying, and fresh-meal preparation-will increasingly determine energy intensity and long-term margin resilience.

Competitive Landscape: Clinical Credibility and Portfolio Expansion

Competition is intensifying as leading multinationals strengthen science-led positioning and expand premium portfolios.

Major players such as Nestlé Purina Pet Care, Mars Petcare, Hill's Pet Nutrition, The J.M. Smucker Company, and General Mills are leveraging acquisitions, veterinary partnerships, and personalized nutrition programs to reinforce brand differentiation.

Industry consolidation, specialty-retail penetration, and direct-to-consumer subscription models are reshaping channel strategy. FMI analysis suggests future share gains will favor companies capable of:

Demonstrating clinical outcomes

Maintaining ingredient transparency

Aligning sustainability claims with verifiable metrics

Executing seamlessly across e-commerce and brick-and-mortar retail

Market Snapshot (2026-2036)

Metric | Value |

Industry Size (2026) | USD 54.3 Billion |

Industry Value (2036) | USD 97.4 Billion |

CAGR | 6.0% |

Leading Source | Animal-Derived (38.2%) |

Dominant Product Type | Kibble (42.6%) |

Leading Distribution Channel | Pet Stores (35.4%) |

The Outlook: From Premium Option to Nutritional Standard

By 2036, dog food will increasingly be evaluated not merely on flavor or brand equity, but on validated digestibility, measurable functional outcomes, and documented compliance performance. As pet ownership deepens and veterinary oversight tightens, science-backed, premium-positioned nutrition will transition from discretionary upgrade to industry standard.

The dog food market's trajectory toward USD 97.4 billion reflects more than volume growth-it signals a structural shift toward disciplined formulation, regulatory alignment, and outcome-driven value creation across the global canine nutrition ecosystem.

For an in-depth analysis of evolving formulation trends and to access the complete strategic outlook for the Dog Food Market through 2036, Full Report Request - https://www.futuremarketinsights.com/reports/dog-food-market

Related Reports:

Dog Food and Snacks Market: https://www.futuremarketinsights.com/reports/dog-food-and-snacks-market

Dog Food Topper Market: https://www.futuremarketinsights.com/reports/dog-food-toppers-market

Vegan Dog Food Market: https://www.futuremarketinsights.com/reports/vegan-dog-food-market

Cat and Dog Food Topper Market: https://www.futuremarketinsights.com/reports/cat-and-dog-food-toppers-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales - [email protected]

For Media - [email protected]

For web - https://www.futuremarketinsights.com/

SOURCE: Future Market Insights, Inc.

Information contained on this page is provided by an independent third-party content provider. XPRMedia and this Site make no warranties or representations in connection therewith. If you are affiliated with this page and would like it removed please contact [email protected]